Downpayments need to be substantial because the owner needs to have skin in the game. Otherwise the borrower could walk away from the house and the mortgage with very little downside.

The whole point of interest is supposed to account for that risk.

People buy cars all the time that cost a decent fraction of what a house does, and nobody bats an eye when they finance 100% (or more) of the value. And a car depreciates and moves. The bank knows where to find the collateral for a mortgage, and the value generally appreciates.

We had a whole, massive global financial crisis that was essentially caused by the fact that this does not work for housing because the risks are so heavily correlated: a large chunk of society finds that they cannot afford the downpayments and defaults all at once, which causes house prices to decrease and the economy to collapse, which in turn means that more people default on their mortgages. It's a systemic risk that affects everyone and that the markets alone do not protect against, which is why regulators have cracked down on mortgage lending so strongly.

No, we didn't have a global financial crash because a few poor people couldn't pay their mortgage. We had that crash because some people gambled huge amounts of other people's money on whether these mortgages would be paid.

I used to write some lengthy posts about this and then a few months ago The Big Short was on TV, I watched it for the first time, and realised it was saying exactly what I'd been trying to explain for years. So just watch that.

Plus it has Margot Robbie explaining the technical terms in a bubble bath, so if you don't get it the first time, you can rewind and watch again.

the problem isn't not requiring 20% down. the problem is not setting interest rates appropriately. the banks did a calculation of interest based on housing prices growth, but if you just do the calculation with stagnation/minor depreciation you get an appropriate interest rate for the lower collateral

Someone walking away from a house doesn’t destroy the house.

The lender’s risk is therefore limited to the difference between purchase price and actual value of the property. Which is something they can hedge or simply not make a loan if they think the property is wildly overvalued.

>Someone walking away from a house doesn’t destroy the house.

The experience of the foreclosure crisis seems to differ. I know people who moved into houses where holes were punched into walls and everything was removed that could be, from door knobs to outdoor deck planks.

You describe damage to a property that a bank owns. Therefore the costs fall on the bank. This is part of the definition of the concept of "taking on risk" and if banks are not accounting for these outcomes in their business model, they're simply bad at business.

This is only true for a federally backed mortgage. Yes, down payment levels, in the context of whether someone needs mortgage insurance, is set by regulation. But down payments can be much less significant if you’re ok with mortgage insurance. Down payments required by banks were typically higher before regulation.

Before regulation it really depended on the buyer. Some people where putting down 5% without insurance, others had much stricter requirements.

We’ve settled on a really arbitrary system where for example the Federal Housing Administration requires huge upfront FHA insurance payments without regard for down payment size if it’s less than 20%. If you’ve saved up say a 8% down payment you really should be a significantly lower risk than someone putting down 3.5%.

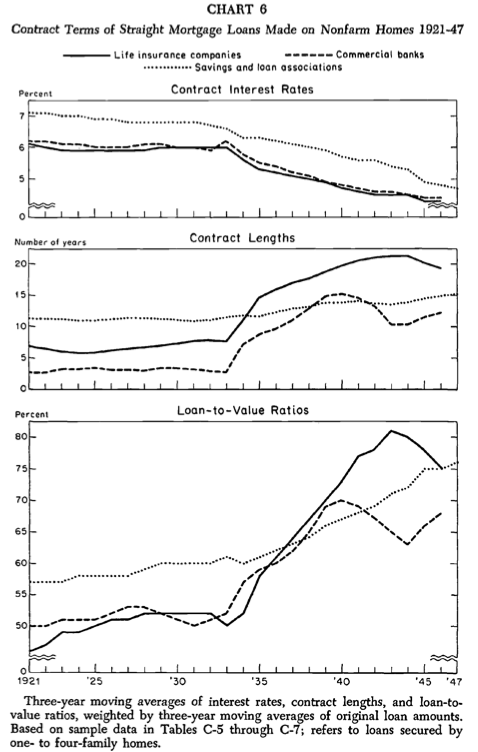

The buyer wasnt the decider. The bank was because they were the one taking the risk. The down payment required by banks before regulation was often 30% or more. That’s partly why home ownership was much lower prior to WW2.

I suspect we’re looking at this through different temporal lenses. When I talk about regulation, I mean the last 100 years in its entirety, not just since the financial crisis of 2008. I agree with some of your point regarding how thresholds are set arbitrarily, though.

> The down payment required by banks before regulation was often 30% or more.

I am talking about lending before regulation. High down payments were not universally applied, so yes sometimes a loan might require 40% but other borrowers might offer nothing. My point is you can’t simply say the required amounts were excessively high some of the time because they weren’t universal and selected based on a perception of risk.

Yes (except in the cases of short sales, where I’ve seen the same). My point was not about who assumes that risk, just pushing back on the idea that people wouldn’t damage a house they were going to be forced out of.

A down payment of 20% provides some of that exact cushion (and makes it less likely for a borrower to casually walk away from a house that fell in value or was otherwise a poor purchase).

Any regard is a really low standard, minimal is more accurate. You don’t end up with nice round numbers like 20% which never changes due to economic conditions etc from calculating some formula.

The global range is wider than that and reflects the reasonable range of this kind of regulation. If it’s say 75% then what’s the point of a loan? On the other hand if it’s 1% what’s the point of the regulation?

Regulators are basically picking a number between 3.5% to 35% and 20% is a nice round number in the middle of that range.

That's a much better reason, or, at least, something to respond to. Thank you.

Accountability on the part of the prospective owner can be achieved in multiple ways, but using down payments probably minimizes the amount of bureaucracy and following-up in how authorities manage this kind of thing.

Of course, implementing it this way creates "structural inequity", i.e., a process that inherently separates one group into two groups along lines that members of that group have little to no control over. Obviously the property not-having-money is correlated with other factors such as skin color and whether your parents went to college, which creates divisions along lines that are not just economic but socio-economic, and influence the development of not just that person but also everyone who depends on that person, including future generations.

I would be very interested to hear more from systems theorists on other kinds of methods that don't reproduce these kinds of correlated outcomes.

Hierarchies need hierarchy. Economic apartheid is one of the most common - and least questioned - ways to enforce hierarchy.

It's the usual problem of defining the difference between a progressive and a regressive economy. Regressive economies claim to be about "freedom" but in practice it's a very selective freedom that benefits a few small sectors and acts as a brake on innovation, development, and entrepreneurship for everyone else.

Consider all the businesses that could have been started by talented people currently spending all of their income on rent. It's a brittle, oppressive outcome.

Progressive economies rely on wealth redistribution to create something closer to a genuine meritocracy.

There's a whole PR industry devoted to denying this, but it's not a coincidence that the US was a powerhouse of innovation when redistributive taxes were at their highest. And has stagnated as economic apartheid has become more entrenched.

That's the crux of the political debates going on today. What kinds of values are represented by the status quo, and what kinds of values may replace a (retrospectively) naive approach to meritocracy.

The owner does have skin in the game. It's their home. If the down payment is too high, many people are prevented from owning a home. This causes these people to be stuck in the rental trap, paying >2x what a mortgage payment would cost. Good for landlords & those in the rental industry, bad for everyone else.

There is no rental trap. The problem is runaway inflation that destroys savings and taxes investment gains. The only reason housing is such a good deal is that the first 500k is tax free.

Your decree does not invalidate the lived experiences of the people who want to own a home but can't afford the > $80k down payment, so they are stuck paying rent. The problem is credit inflates housing prices. Some parties, such as speculators, have plenty of credit, so they can buy multiple houses & inflate the markets using credit. Those who cannot obtain credit or are not willing to play the game are stuck trying to save up > $80k for the down payment on top of their regular living expenses that are under rapid inflation.

The middle class used to be able to buy a home or large acreage outright without credit.

They don't have skin in the game if they borrow 100% of the value of a house - house drops 20% in value, they just return the keys and walk away - heads I win, tails you lose. Banks don't want to play that game and I can't blame them.

Who would want to walk away from their home? The people living on the streets perhaps?

Credit inflates the housing markets. Houses used to be bought outright without credit. Credit is top heavy, where a small number of parties can obtain enough credit to buy many houses while an increasing amount of people cannot obtain credit to buy a house to live in. The people who already own property benefit from increasing valuations, while people entering into the housing market bear the costs. It's gotten to the point to where people with 6 figure incomes cannot afford a house.

It seems like the instability of the housing prices is largely due to the volatility of credit markets. If housing was not emphasized as an appreciating asset class to be hoarded by speculators who want to grow rich from housing, then more people, who are now stuck in the rental trap, can live in their own home. The situation we have now is that non-speculators who want to own a home have to bear the risk of a credit inflated & volatile asset when all they want to do is own a house & not pay > 2x rental costs. Those who do successfully play the game now live with neighbors who also play the game, instead of a more diverse crowd of people they would rather be neighbors with. The banks created & profit from this mess & are bailed out. The non-speculating aspiring home owner pays the costs.

You're describing a "heads I win, tails you win" situation with no down payment. If the house drops in value, the borrower walks away and "wins". If the house appreciates in value, the borrower stays and the bank receives X% interest, on time, in full, for 30 years and "wins."

... meaning that they did not have a substantial downpayment. Assuming they bought in Washington state, they probably also had a non-recourse mortgage.

{kind=link}